Get a Quote

Get a Quote pay online

pay online hello@dudgeonberry.com.au

hello@dudgeonberry.com.au 02 6621 3000

02 6621 3000

Is My Property in a Flood Zone? How to Check and What It Means for Your Insurance

A Comprehensive Guide for Australian Property Owners

Table of Contents

- Why Understanding Flood Zones Matters

- What is a Flood Zone?

- How to Check if Your Property is in a Flood Zone

- Understanding Australian Flood Risk Categories

- What Your Flood Zone Means for Insurance

- Steps to Take if You’re in a Flood Zone

- Common Flood Zone Myths Busted

- Frequently Asked Questions

Why Understanding Flood Zones Matters

Whether you’re buying a new home, reviewing your current insurance coverage, or simply want peace of mind, understanding your property’s flood risk is one of the most important aspects of property ownership in Australia. With climate patterns shifting and extreme weather events becoming more frequent, knowing whether your property sits in a flood zone can help you make informed decisions about insurance, property improvements, and emergency preparedness.

For many Australians, flood awareness isn’t just theoretical – it’s essential. Recent flooding events across Brisbane, the Gold Coast, Sydney’s Western suburbs, and regional areas throughout Queensland, New South Wales, and Victoria have demonstrated just how quickly flood waters can impact communities, even in areas where flooding hadn’t occurred in living memory.

The financial impact of flooding without adequate insurance can be devastating, with average flood damage claims ranging from $50,000 to well over $100,000 for residential properties. Understanding your flood zone status is the first step in protecting your most valuable asset.

What is a Flood Zone?

A flood zone is a designated area identified by government authorities and hydrological experts as having a measurable risk of flooding. These zones are determined through extensive analysis of:

- Historical flood data spanning decades or even centuries

- Topographical surveys that map land elevation and natural drainage patterns

- Hydrological modeling that predicts water flow during various rainfall scenarios

- Climate projections accounting for changing weather patterns

- Urban development impacts on natural water systems

Flood zones aren’t simply “yes or no” designations. They exist on a spectrum from minimal risk to high probability flooding areas, helping property owners, insurers, and local councils make informed decisions about development, safety, and financial protection.

It’s important to note that flood zones can affect properties far from major rivers or coastlines. Urban areas with inadequate stormwater systems, low-lying suburbs near creeks, and even hillside properties with poor drainage can all fall within flood planning areas.

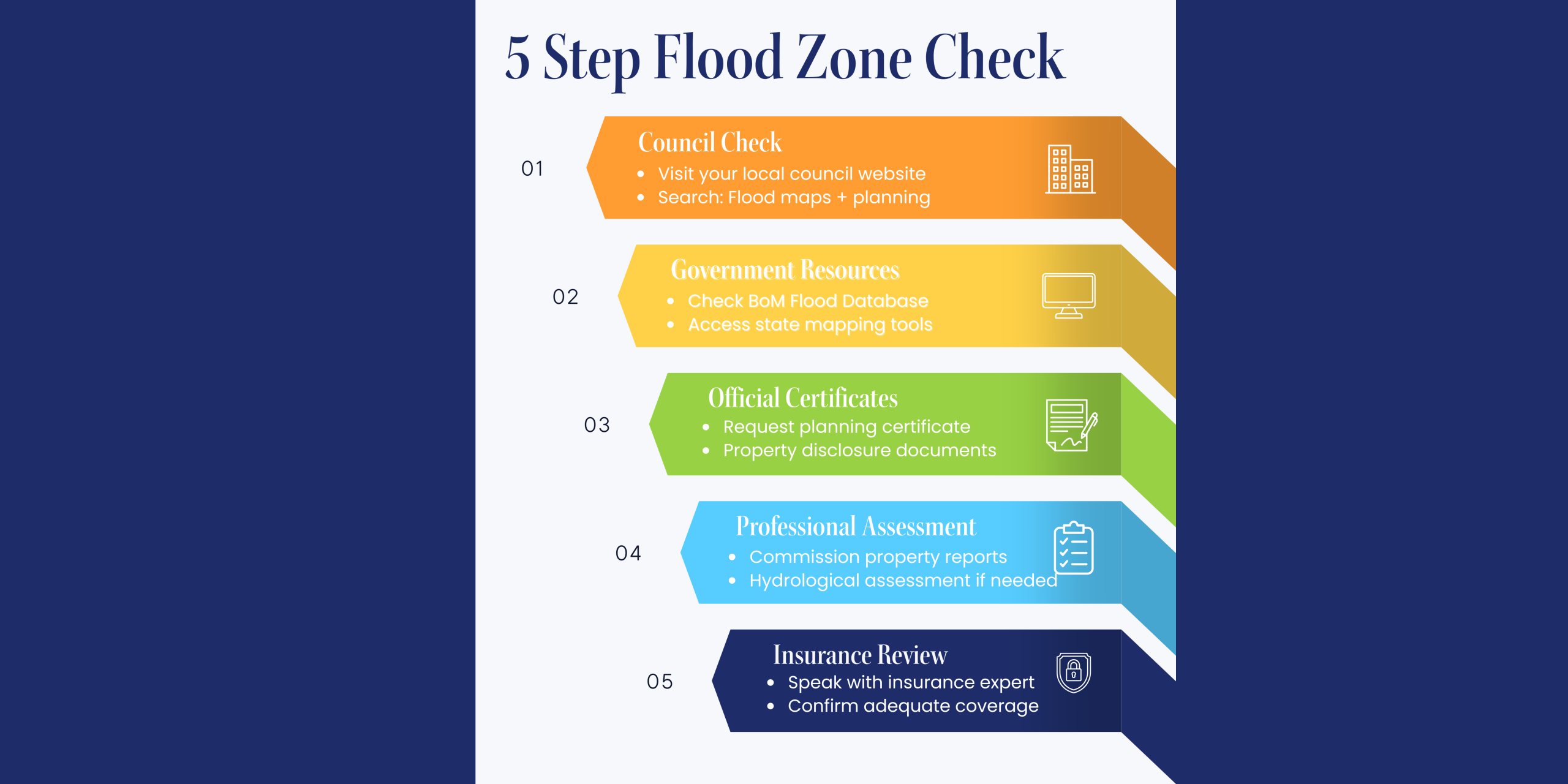

How to Check if Your Property is in a Flood Zone

Determining your property’s flood risk involves checking several authoritative Australian resources. Here’s your step-by-step guide:

1. Check Your Local Council’s Flood Maps

Your local council maintains the most detailed flood planning information for your specific area. Visit your council’s website and search for:

- Flood planning maps

- Flood studies

- Development control plans (DCP)

- Flood risk management plans

Most councils now offer interactive online mapping tools where you can enter your address and instantly see flood overlays. Major city councils including Brisbane City Council, Gold Coast City Council, City of Sydney, and Melbourne City Council all provide comprehensive online flood mapping.

2. Use the National Flood Information Database

The Australian Government’s Bureau of Meteorology provides access to flood information across Australia. Their website offers:

- Historical flood records

- Known flood-prone areas

- Flood warning systems for your region

- River height data and flood classifications

3. Access State Government Resources

Each state offers specific flood information tools:

New South Wales:

- NSW Spatial Services’ SEED Portal (Sharing and Enabling Environmental Data)

- NSW State Emergency Service (SES) FloodSafe website

- Planning Portal NSW for flood planning information

Queensland:

- Queensland Globe mapping tool

- Queensland Reconstruction Authority flood maps

- QFlood database for flood study information

Victoria:

- Victorian Floodplain Management Strategy resources

- Water.vic.gov.au flood information

- Victorian Planning Authority flood overlays

South Australia:

- SA Water flood mapping

- DEW (Department for Environment and Water) flood resources

Western Australia:

- Department of Water and Environmental Regulation flood mapping

- Local government flood studies

Tasmania & Northern Territory:

- Check your state’s emergency services or water management authority websites

4. Request a Section 10.7 Certificate (NSW) or Equivalent

When purchasing property, always obtain:

- Section 10.7 Certificate (formerly Section 149) in NSW

- Property Information Certificates in Queensland

- Vendor Statements (Section 32) in Victoria

- Property Disclosure Statements in other states

These official documents disclose whether the property is affected by flood planning controls, though they may not always show historical flooding.

5. Review Property Purchase Reports

Professional property reports often include flood risk assessments. Consider commissioning:

- Building and pest inspections that note flood evidence

- Surveyor reports showing elevation levels

- Hydrological assessments for high-risk areas

- Environmental reports that identify water-related risks

6. Talk to Locals and Real Estate Agents

While not a substitute for official data, long-term residents can provide valuable insights about historical flooding events that may not appear in official records. Ask about:

- Previous flood events and their severity

- How quickly water rises in the area

- Seasonal flooding patterns

- Which streets or areas are most affected

Understanding Australian Flood Risk Categories

Australian flood planning typically categorises risk into several levels. While terminology varies by council, here’s a general framework:

| Flood Risk Category | Description | Typical Implications |

|---|---|---|

| Flood Planning Area (FPA) | Area affected by floods up to the Probable Maximum Flood (PMF) | May require flood-aware building design; insurance may be available with conditions |

| High Flood Risk Precinct | Areas subject to regular flooding or deep/fast-flowing floods | Significant building restrictions; insurance often difficult or expensive to obtain |

| Medium Flood Risk | Areas where flooding is less frequent or less severe | Some building controls apply; insurance generally available but may have higher premiums |

| Low Flood Risk | Minimal flood probability based on historical data | Few restrictions; standard insurance coverage typically available |

| Flood Free/Minimal Risk | Above the PMF or no recorded flood history | No flood-related building controls; standard insurance rates apply |

Important Note: These categories can change as new flood studies are completed or climate patterns evolve. A property that was considered low risk a decade ago may now be classified as medium risk due to updated modelling or increased urban development affecting drainage.

What Your Flood Zone Means for Insurance

Understanding your flood zone directly impacts your insurance options and costs. Here’s what you need to know:

Standard Home and Contents Insurance

Most Australian home and contents insurance policies include flood cover as standard, but there are critical details to understand:

- Policy definitions matter: Insurance companies use specific definitions of “flood” that may differ from common understanding. Typically, flood means water escaping from a natural watercourse, lake, or the sea.

- Excess amounts: Properties in known flood zones typically carry higher excess amounts for flood claims. These will vary by location and level of risk.

- Premium costs: Flood-prone properties command higher premiums, sometimes 2-3 times standard rates.

- Coverage limits: Some insurers cap flood damage payments or exclude certain items like landscaping or retaining walls.

What’s Considered a “Flood” vs Other Water Damage

Understanding insurance definitions is crucial:

- Flood: Water escaping from rivers, creeks, lakes, or the sea

- Storm damage: Wind-driven rain entering through damaged roofs or windows

- Rainwater runoff: Water flowing over the ground surface (may not be covered under all policies)

- Stormwater: Water from overwhelmed drainage systems (coverage varies)

Strata Insurance Complexities

For apartment and townhouse owners, flood coverage sits within strata insurance:

- Individual owners should verify what the strata policy covers

- Contents insurance remains your personal responsibility

- Flood damage to common property is typically covered under strata policies

- High-rise buildings may have different risk profiles than low-rise complexes

When Insurance May Not Be Available

In extreme high-risk areas, some insurers may:

- Decline to offer flood coverage

- Exclude flood from policies entirely

- Offer coverage with prohibitively high premiums or excesses

- Limit coverage to partial replacement rather than full rebuild

The Importance of Full Disclosure

When applying for insurance, you must disclose:

- Knowledge of flood zoning or flood planning overlays

- Previous flood damage to the property

- Proximity to waterways, creeks, or drainage channels

- Council flood planning controls affecting your property

- Any flood mitigation measures you’ve installed

Failure to disclose can result in claim denial, even for non-flood-related claims.

Steps to Take if You’re in a Flood Zone

Discovering your property is in a flood zone doesn’t mean disaster, it means taking informed action:

1. Review Your Current Insurance

Contact your insurance broker or provider immediately to:

- Confirm flood coverage is active and adequate

- Understand your excess and coverage limits

- Discuss mitigation measures that might reduce premiums

- Ensure your sum insured reflects current replacement costs

- Compare quotes from multiple insurers specializing in flood-prone properties

2. Develop a Flood Emergency Plan

Create a household flood plan that includes:

- Emergency contact numbers (local SES, family members, insurance broker)

- Evacuation routes and meeting points

- Critical documents stored in waterproof containers or digitally backed up

- Essential items ready to grab quickly (medications, valuables, photos)

- Plans for pets and livestock

- Knowledge of your home’s highest point for moving belongings

3. Consider Property Modifications

Flood-proofing measures can reduce risk and potentially lower insurance costs:

- Raise electrical outlets, switchboards, and appliances above potential flood levels

- Install flood-resistant materials on lower floors (tiles instead of carpet, water-resistant wall materials)

- Improve drainage around your property with appropriate grading

- Install backflow prevention devices on sewage and stormwater connections

- Consider flood barriers, flood gates, or elevated foundations

- Elevate valuable items and store them on upper floors

- Install sump pumps in low-lying areas

4. Stay Informed

- Register for your local council’s flood warning system

- Download the SES or emergency services app for your state

- Monitor weather forecasts during storm seasons (typically October-April in northern Australia)

- Understand local flood classifications (minor, moderate, major)

- Know the difference between flood watch, flood warning, and evacuation orders

- Join community emergency preparedness groups or neighborhood networks

5. Maintain Regular Insurance Reviews

Meet with your insurance adviser annually to:

- Update your coverage as property values change

- Review recent flood studies or zone changes in your area

- Ensure you’re adequately covered for rebuilding costs including demolition and site clearing

- Explore premium reduction strategies through mitigation measures

- Check if your insurer offers discounts for flood-resistant improvements

Common Flood Zone Myths Busted

Myth 1: “My property hasn’t flooded in 50 years, so I’m safe.”

Reality: Climate change is altering historical patterns. The 2022 floods across Queensland and NSW affected areas that hadn’t flooded in recorded history. Areas that were once safe may now be at risk. Always check current flood mapping.

Myth 2: “Flood insurance is optional in Australia.”

Reality: While you can technically decline it, doing so leaves you financially exposed to potentially catastrophic losses. With average flood claims exceeding $50,000, it’s a risk most property owners cannot afford.

Myth 3: “If I’m not near a river, I can’t flood.”

Reality: Overland flow flooding can occur anywhere when drainage systems are overwhelmed. Properties in Brisbane’s western suburbs, Melbourne’s inner-city areas, and Sydney’s Eastern suburbs have all experienced flooding despite being kilometers from major waterways.

Myth 4: “Standard home insurance doesn’t cover floods.”

Reality: Most Australian policies now include flood cover as standard following regulatory changes in 2013, though the definition of “flood” and coverage limits vary between insurers.

Myth 5: “If my property is in a flood zone, I can’t get insurance.”

Reality: While challenging in extreme cases, most flood-zone properties can obtain coverage, though at higher premiums. Specialist brokers like Dudgeon Berry Insurance Group can help find coverage even for difficult properties.

Myth 6: “All water damage is covered the same way.”

Reality: Insurance distinguishes between flood, storm damage, and rainwater runoff. The cause of water damage determines whether and how it’s covered.

Myth 7: “Apartments on upper floors don’t need flood coverage.”

Reality: While your unit may not flood directly, common property damage affects all owners through strata insurance costs, and you may lose access to your home during flooding events.

Frequently Asked Questions

We’ve put together a comprehensive list of the most frequently asked questions we receive when it comes to flood insurance.

Is flood information publicly available for any Australian property?

Yes. Council flood maps, planning certificates, and state government databases provide public access to flood risk information for most Australian properties. However, the level of detail varies between councils.

How often do flood zone maps get updated?

This varies by council. Major updates typically occur after significant flood events or every 5-10 years when new flood studies are completed. Some councils in rapidly developing areas update more frequently. Always check the date on any flood map you’re reviewing.

Will being in a flood zone affect my property value?

Potentially, yes. Properties in known flood zones typically sell for 5-20% less than comparable properties outside flood zones, with the discount increasing significantly after recent local flood events.

Can I challenge my property’s flood zone classification?

Yes. If you believe your property has been incorrectly classified, you can commission an independent hydrological assessment and present evidence to your local council. However, official reclassification processes are complex, costly, and not always successful.

What’s the difference between a 1-in-100-year flood and a 1-in-20-year flood?

These terms refer to probability, not frequency. A 1-in-100-year flood (also called the 1% Annual Exceedance Probability or AEP flood) has a 1% chance of occurring in any given year and represents a more severe flooding event. A 1-in-20-year flood has a 5% chance annually and is typically less severe. Confusingly, you could experience multiple “1-in-100-year” floods within a short period – the term describes probability, not a guaranteed timeframe.

Does flood zone designation mean my property will definitely flood?

No. It indicates probability and risk based on modeling and historical data. Many properties in flood zones never experience actual flooding, while some properties outside mapped zones can flood due to unexpected circumstances or inadequate drainage infrastructure.

What should I do if I’m buying a property in a flood zone?

Before purchasing, obtain professional advice including independent building inspections, flood risk assessments, and definitive insurance quotes. Factor potential insurance costs (which could be $2,000-$5,000+ annually) into your budget, and negotiate the purchase price accordingly. Never assume you can obtain affordable insurance without confirming it first.

Are there government grants available for flood mitigation?

Some state and federal programs offer grants for flood resilience measures, particularly after declared disaster events. The Australian Government’s Disaster Ready Fund and various state-based programs provide funding for community flood mitigation. Check with your state’s emergency services or reconstruction authority for current programs.

Does flood insurance cover temporary accommodation if my home is uninhabitable?

Most comprehensive policies include “alternative accommodation” or “additional living expenses” coverage, but there are limits (typically 10-20% of your building sum insured or 12-24 months). Check your policy details carefully.

What if I can’t afford flood insurance for my property?

Speak with an experienced insurance broker who can help you explore options including higher excesses to reduce premiums, government assistance programs, or specialist insurers who may offer more competitive rates. Never go without insurance – the financial risk is too great.

Take Control of Your Flood Risk Today

Understanding your property’s flood zone status is a crucial step in protecting your most valuable asset. Whether you’re in Sydney, Melbourne, Brisbane, the Gold Coast, Adelaide, Perth, regional Australia, or anywhere in between, having the right information empowers you to make smart decisions about insurance, property improvements, and emergency preparedness.

At Dudgeon Berry Insurance Group, we’ve helped Australian property owners navigate complex flood insurance scenarios for the last 3 decades including the devastating 2022 Northern NSW floods. With offices serving Northern NSW, the Gold Coast, and clients Australia-wide, our expertise in regional and metropolitan flood risks, combined with our commitment to professional advice and personal service, means we’re here to find the right coverage for your unique situation, no matter where your property is located.

Need help understanding your flood insurance options? Contact our team today for a comprehensive review of your property insurance needs. We’ll help you secure the protection you need at a price that works for your budget, whether you’re in a high-risk flood zone or simply want peace of mind.

This article provides general information only and should not be considered personal advice. Flood zones, insurance requirements, and regulations vary significantly by location and individual circumstances. Always seek professional advice specific to your situation from qualified insurance advisers and local authorities.